Effective Strategies to Reduce Debt in Times of Crisis

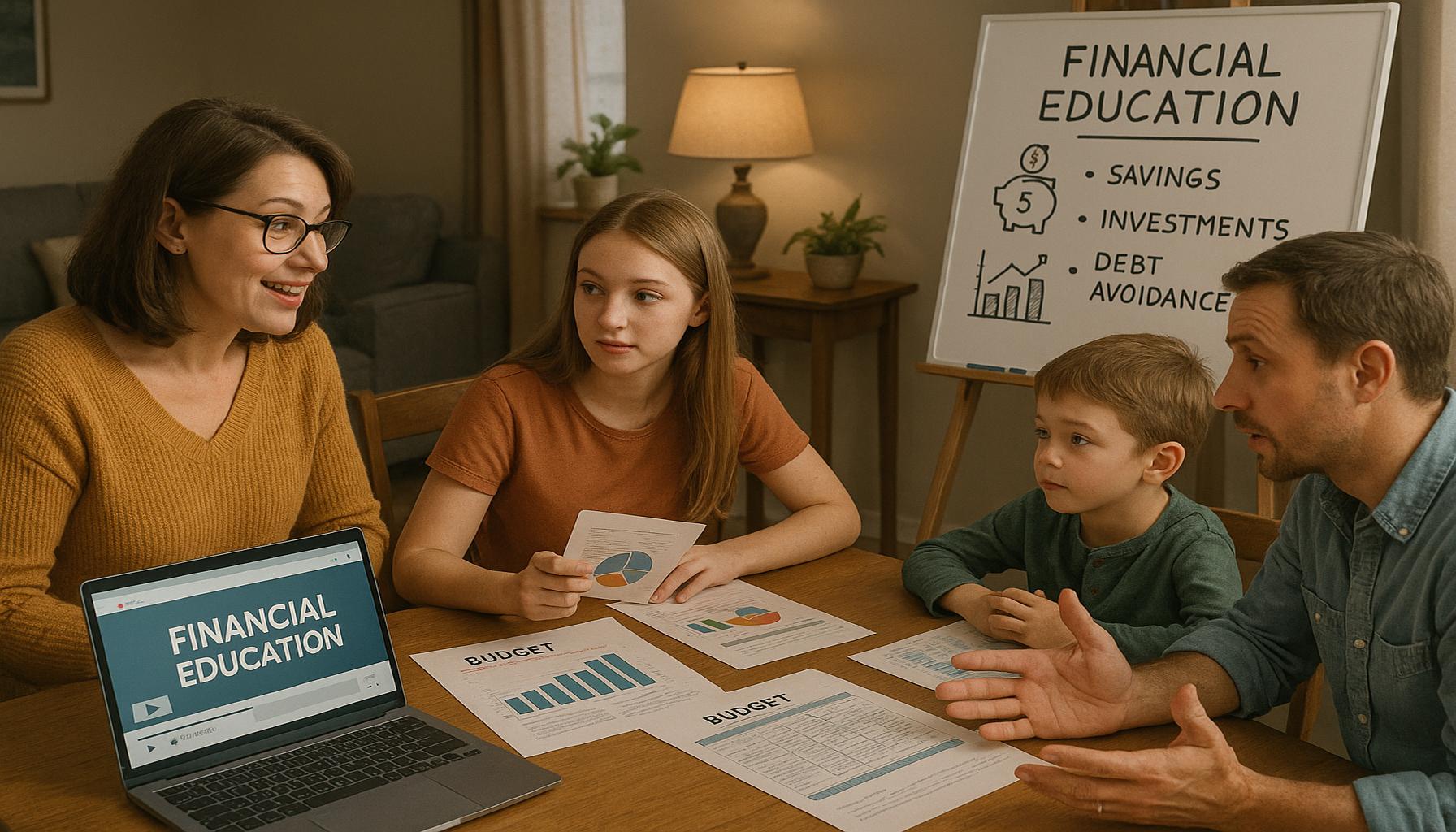

Understanding Debt Management in Tough Times

Experiencing financial strain can feel daunting, especially when there are numerous obligations to fulfill. For many Canadians, the unsettling reality of crisis can manifest in various forms, making it critical to develop effective strategies to alleviate these pressures. The situation can feel helpless, yet with the appropriate tactics, there is hope for recovery and a return to financial stability.

During periods of crisis, several factors can contribute to the deterioration of financial health:

- Job loss or reduced income: It’s not uncommon for individuals to face sudden layoffs or reductions in work hours. For instance, many in the service industry were forced to confront these challenges during the pandemic, which has left lasting effects on job security.

- Increased living costs: Essential expenses such as housing, utilities, and groceries often see sharp increases, particularly in regions like Vancouver or Toronto where high costs can stretch budgets thin.

- Market fluctuations: Canadians who invest in the stock market may find their portfolios damaged amid economic downturns, leading to additional stress and concern about retirement savings and future financial stability.

However, understanding and implementing practical strategies can help individuals navigate through these challenging moments and regain a sense of control over their finances:

- Budgeting: Creating a budget is foundational to managing debt effectively. By meticulously tracking income and expenses, individuals can identify which areas are critical and which can be cut back. Apps like Mint or YNAB (You Need A Budget) can aid in this process, ensuring that every dollar has a purpose.

- Negotiation: Open communication with creditors can lead to more manageable payment terms. Many lenders offer hardship programs that can lower monthly payments or temporarily suspend them, providing much-needed relief during difficult periods.

- Seeking professional advice: Consulting with financial advisors or debt relief services can provide tailored solutions designed specifically for each individual’s circumstances. Many organizations across Canada offer free consultations, making this an accessible option for those overwhelmed by their debts.

In conclusion, while navigating financial hardships can be undeniably challenging, implementing calculated strategies provides a route to recovery. By building a robust financial plan, engaging with creditors, and seeking professional guidance, individuals can not only reduce their debts but also emerge from the crisis with a clearer understanding of their financial habits. Strength and resilience are cultivated in these trying times; thus, with determination, one can transform financial struggles into a stepping stone toward a more secure future.

DISCOVER MORE: Click here to learn how to apply

Smart Practices for Financial Resilience

As the financial landscape shifts unpredictably during a crisis, careful navigation becomes essential for preserving economic health. In Canada, where many households already operate on tight budgets, the urgency to respond effectively to financial upheavals cannot be overstated. Individuals and families must arm themselves with strategies that not only address immediate debt concerns but also foster long-term financial resilience.

One of the most effective weapons in this battle is budgeting. Taking a meticulous approach to tracking finances enables individuals to see exactly where their money is flowing. By listing all sources of income against monthly expenditures, one can pinpoint unnecessary expenses that can be curtailed. For instance, during challenging times, many find that subscriptions to streaming services or frequent dining out can be paused or eliminated altogether. Furthermore, utilizing budgeting apps like Mint or YNAB can simplify this process by providing visual insights and alerts about spending habits. Through diligent management of daily finances, one can create breathing room within their budget to start repaying debts more aggressively.

Another essential strategy is the art of negotiation. Many creditors are acutely aware of the circumstances driving individuals into financial distress. This openness provides an opportunity for debtors to reach out and initiate dialogue. By communicating openly about one’s situation, individuals may discover that lenders offer hardship programs or flexible payment plans to ease the burden. In fact, the Canadian Mortgage and Housing Corporation (CMHC) recommends reaching out to lenders promptly to explore options and negotiate terms that align better with one’s current financial capability.

In addition to personal budgeting and negotiation, seeking professional advice can be a transformative step. Financial advisors bring expertise that can tailor solutions to individual needs. For many Canadians, organizations such as Credit Canada or the Canadian Association of Credit Counselling Services offer valuable resources and free consultations to help guide people in financial distress. These professionals can work with individuals to identify debt management plans that fit personal circumstances, providing a roadmap to recovery while imparting knowledge on sustainable financial practices.

Moreover, staying informed about government aid programs can be pivotal. In times of crisis, federal measures may provide temporary relief, such as income support, rent assistance, or loan deferral options. Each of these resources can serve as essential lifebuoys amid a turbulent financial sea, enabling those affected to maintain their stability while strategizing their path forward.

Ultimately, by relying on disciplined budgeting, enterprising negotiation, and expert guidance, individuals can carve a path through financial challenges. Each of these strategies empowers Canadians to not only face debts head-on but also to emerge from crisis situations with renewed confidence and financial acumen. In transformative times, resilience is built through informed action, allowing one to regain control and set sights firmly on a brighter financial future.

DISCOVER MORE: Click here for details on applying for the National Bank MC1 Mastercard

Building a Supportive Financial Network

As individuals grapple with their financial reality during times of crisis, the importance of building a supportive financial network cannot be understated. Engaging with family, friends, and close acquaintances fosters a space where individuals can share experiences, gather insights, and even verbalize their financial struggles—a process that can lead to valuable advice and assistance. Open conversations regarding financial challenges can demystify debt and reduce the shame often associated with it. Many may find that they are not alone in their situation, and this shared vulnerability can lead to a stronger collective strength.

Within this network, individuals can explore options such as group buying activities, shared resources, or even joint budgeting. For example, pooling together for bulk purchases or shares for communal meals can significantly lower costs for everyone involved. It exemplifies community spirit while cutting down on the individual burden of debt. Additionally, local community groups or online forums often offer an abundance of knowledge about optimizing spending, budgeting, and debt management—all rooted in shared local experiences.

Creative Solutions for Debt Reduction

Diversifying income sources also serves as a vital strategy amidst crisis—especially for those whose jobs may be unstable or furloughed. By exploring side gigs or freelance opportunities, individuals can supplement their income, thereby providing them with more funds to tackle outstanding debts. Platforms like Upwork and Fiverr open doors to opportunities ranging from graphic design to content writing that can help those with specialized skills monetize their talents. Furthermore, local job boards may offer part-time or short-term employment options that could provide the financial boost necessary to alleviate immediate debt pressures.

Moreover, examining current assets can present unconventional methods for debt repayment. For instance, consider selling items that have outlived their usefulness or are no longer needed through apps like Kijiji or Facebook Marketplace. Not only does this declutter your living space, but it can also yield quick cash that can be applied towards paying down debts. Additionally, many Canadians possess skills or hobbies that can be transformed into income-generating endeavors. Whether it’s baking, crafting, or tutoring, tapping into one’s passions can open new revenue streams during times of financial strain.

Leveraging Technology and Resources

In today’s digital landscape, leveraging technology is another critical component in effective debt management. Various personal finance tools and resources can help users visualize and systematically tackle their debts. Using apps that track spending habits enables individuals to make instantaneous decisions and adjustments instead of waiting until the end of the month to assess their financial health. Furthermore, financial literacy websites and podcasts offer insights into debt management strategies, ensuring individuals are equipped with the necessary knowledge to make informed decisions.

Finally, understanding the scope of personal debt is essential. Taking the time to classify debts—whether they are high-interest credit card debts or lower-interest student loans—can guide individuals to prioritize effectively. Paying off high-interest debts first can save substantial amounts over time, allowing individuals to restructure their repayment approach in a way that reduces financial stress more efficiently.

As each Canadian faces their unique struggles, implementing a combination of community support, creative strategies for additional income, and utilizing technology will fortify their ability to overcome debt challenges. Through these informed approaches, individuals can not only alleviate current debts but also foster a culture of ongoing financial awareness and resilience.

DON’T MISS: Click here to get the complete guide

Conclusion

In conclusion, navigating through debt during times of crisis requires a multifaceted approach that merges community support, innovative income generation, and technological resources. Individuals who cultivate a supportive financial network can find comfort and guidance in shared experiences, reducing feelings of isolation. By engaging in open discussions about financial challenges, bonds can strengthen, fostering collective resilience against the burdens of debt.

Furthermore, the exploration of side gigs and freelance opportunities can provide a crucial lifeline for those facing job instability. The act of transforming hobbies into income-generating endeavors not only alleviates financial pressure but also nurtures personal fulfillment. Additionally, embracing the digital age through financial tools empowers individuals to take control of their finances, enabling them to make informed decisions and prioritize effectively based on the nature of their debts.

Ultimately, the journey to financial recovery is not just about alleviating immediate stress; it’s about establishing a sustainable, long-term approach to debt management. As Canadians face new economic challenges, they can emerge stronger and more financially savvy. By combining the power of community, creativity, and technology, individuals can not only reduce their current debts but also build a foundation for a more secure financial future. Now is the time to act, to learn, and to thrive together in the face of adversity.

Linda Carter

Linda Carter is a writer and financial expert specializing in personal finance and financial planning. With extensive experience helping individuals achieve financial stability and make informed decisions, Linda shares her knowledge on the our platform. Her goal is to empower readers with practical advice and strategies for financial success.