The Role of Financial Education in Debt Prevention

Understanding Financial Education

In an era driven by rapid changes and the constant influx of information, managing finances can seem like a daunting task for many individuals. The first step toward achieving financial stability lies in cultivating a deep understanding of financial education. This rich knowledge base goes beyond basic budgeting; it creates a foundation for preventing debt and achieving long-term financial security.

One of the fundamental components of financial education is budgeting. A budget serves as a roadmap for your financial journey, helping you allocate your income toward expenses, savings, and investments. For instance, tools like the 50/30/20 rule suggest using 50% of your income for necessities, 30% for wants, and 20% for savings or debt repayment. Creating a budget isn’t just about tracking spending; it’s about making intentional choices that align with your goals, whether it’s preparing for a vacation or saving for a down payment on a home. This awareness allows Canadians to take control of their finances rather than feeling controlled by them.

Another crucial element is credit knowledge. Understanding how credit scores and credit reports work is vital in today’s economy. In Canada, a strong credit score can significantly decrease borrowing costs, while a poor score may lead to exorbitant interest rates. For example, if a Canadian has a credit score below 600, they might face difficulties securing loans or credit cards. By educating themselves on how to build and maintain a good credit score—such as paying bills on time and keeping credit utilization low—individuals can avoid situations that lead to high-interest debt, ultimately helping them save money in the long run.

Importance of Saving Techniques

Saving techniques also play a pivotal role in fostering financial resilience. Establishing an emergency fund is one of the most effective ways to avoid relying on credit during unexpected situations, such as medical emergencies or job loss. Financial experts often recommend setting aside three to six months’ worth of living expenses in a separate savings account, ensuring that when life throws a curveball, you’re prepared to meet the challenge without accruing debt. In Canada, where the cost of living in cities like Toronto and Vancouver can be quite high, having this financial cushion is increasingly important.

The Broader Impact of Financial Literacy

The impact of financial literacy in Canada cannot be overstated. Many Canadians are burdened with personal debt, with statistics revealing that a significant portion of the population struggles to keep up with payments. By enhancing financial literacy, individuals can develop practical skills like recognizing predatory lending practices. This awareness can prevent them from entering into debt traps where exorbitant fees and interest rates accumulate, ultimately leading to financial distress.

Moreover, setting clear financial goals inspires responsible spending habits. Whether it’s saving for education, a new car, or retirement, having specific targets drives individuals to prioritize their financial decisions. Additionally, a solid understanding of interest rates empowers individuals to explore borrowing options carefully. By comparing rates and terms, Canadians can make smarter borrowing decisions that align with their financial circumstances.

Ultimately, prioritizing financial education is essential for Canadians seeking to achieve financial stability. Taking proactive steps to understand finances not only safeguards against debt but also leads to empowered decision-making throughout life’s journey. By investing time in learning these critical skills, individuals can pave the way towards a stable and prosperous financial future.

DISCOVER MORE: Click here for details

Building a Foundation: The Basics of Financial Education

To truly harness the power of financial education, individuals must first grasp the essential concepts that form the backbone of effective financial management. This understanding encompasses not only core principles such as budgeting and credit knowledge, but also extends to practical financial habits that can protect against overwhelming debt.

At the heart of financial education lies budgeting, often regarded as the cornerstone of financial stability. A well-structured budget acts as an individual’s financial compass, guiding spending and savings decisions. Many Canadians can benefit from employing various budgeting techniques, such as the zero-based budget, where every dollar is assigned a specific purpose, from expenses to investments. This practice cultivates a culture of intentionality, urging individuals to thoughtfully consider each financial decision they make rather than succumbing to impulsive behavior.

The significance of cash flow management cannot be overstated. Monitoring income versus expenses allows individuals to identify patterns in their spending habits. By analyzing these patterns, Canadians can pinpoint areas where they can cut back, redirecting excess funds toward savings or debt repayment. Creating a budget is not merely an academic exercise; it represents a proactive stride toward creating a stable financial future and serving as a powerful preventive measure against debt accumulation.

Understanding the Credit Landscape

Alongside effective budgeting, a solid grasp of credit management is imperative for debt prevention. Credit is a tool that can provide convenience, but it can also become a double-edged sword if mismanaged. Recognizing how credit scores are calculated is vital; factors such as payment history, credit utilization, and the length of credit history come into play. A Canadian with a solid credit score can access loans at favorable interest rates, while someone with a low credit score may face challenges, including higher costs and limited borrowing options.

- Paying bills on time: This habit significantly influences credit scores and portrays financial responsibility.

- Keeping credit utilization low: Using only a portion of available credit can keep scores healthy.

- Diversifying credit types: A mix of credit accounts demonstrates an individual’s capability to manage different debt forms responsibly.

By mastering these elements of credit management, individuals are better equipped to avoid the pitfalls associated with high-interest borrowing. Financial education encourages Canadians to make informed decisions that not only uplift their credit profiles but also shield them against falling into debt’s clutches.

This solid grasp of budgeting and credit knowledge lays the groundwork for another pivotal aspect of financial education—understanding the importance of savings. Building a robust savings plan acts as a safety net that protects individuals from life’s financial shocks. Rather than turning to credit as a first option in emergencies, individuals can draw upon savings to manage unexpected expenses, preventing the feedback loop of accumulating debt.

In summary, embracing financial education equips individuals with the knowledge and skills necessary to navigate the complexities of personal finance. By focusing on budgeting basics and understanding credit dynamics, Canadians can take significant strides towards a debt-free future. The next steps involve implementing practical saving techniques and fostering a financial mindset geared toward long-term security.

DISCOVER MORE: Click here for easy application tips

The Power of Savings and Emergency Funds

While budgeting and credit management form a crucial part of financial education, the importance of savings and creating an emergency fund cannot be understated. The act of saving money is not merely a strategy for future purchases; it serves as a barrier against the accumulation of debt in times of crisis. Emergencies, such as a sudden job loss or an unexpected medical bill, can derail even the most meticulous financial plans. Having a dedicated savings account can mitigate these risks, providing individuals with the flexibility they need in challenging situations.

Financial experts often recommend saving at least three to six months’ worth of living expenses. This buffer equips Canadians to tackle unforeseen expenses without resorting to credit cards or high-interest loans. In fact, building an emergency fund should be one of the first steps in any financial education journey. This reserve ensures that when financial surprises arise, individuals can rely on their savings rather than depleting their credit limits.

Moreover, the discipline of setting aside a portion of one’s income fosters a sense of financial responsibility and control. Engaging in systematic savings—such as automating transfers to a savings account—can make the process easier and more sustainable. Instead of viewing savings as a chore, Canadians can start to embrace it as a vital aspect of their financial well-being.

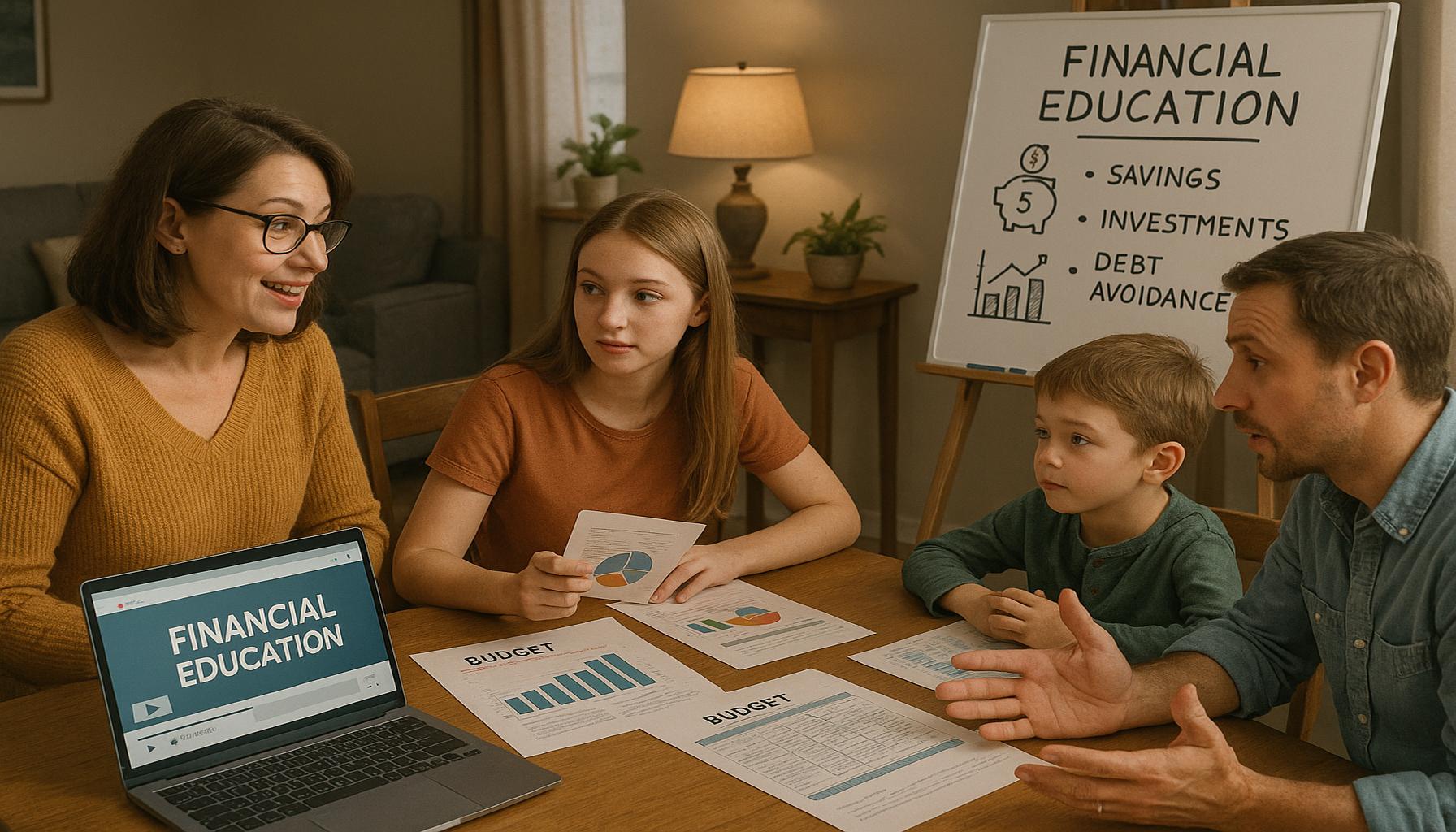

Investing in Financial Literacy Resources

In conjunction with savings, investing in financial literacy resources plays an essential role in big-picture financial education. Local community programs, online courses, and workshops offered by credit unions or financial institutions can provide valuable insights into managing finances effectively. These resources often highlight strategies tailored specifically to the unique economic landscape in Canada, including tax-saving options and government benefits available to citizens.

For instance, many Canadians may be unaware of government programs, such as the Registered Retirement Savings Plan (RRSP) or the Tax-Free Savings Account (TFSA). Understanding how these accounts work and their benefits can encourage individuals to contribute to their financial futures rather than simply focusing on immediate cash flow. Financial education resources can also cover the fundamentals of investment, helping Canadians understand how to grow their wealth and reduce the likelihood of turning to debt in the long run.

Additionally, fostering a habit of ongoing learning in personal finance allows individuals to remain adaptable and informed about changes in the financial landscape. As economic conditions evolve, staying updated on financial literacy can empower Canadians to navigate new challenges effectively, ensuring that they remain in control of their financial destinies.

Making Mindful Financial Choices

One of the most significant aspects of financial education is instilling a sense of mindfulness around financial decisions. In our consumer-driven culture, it’s easy to fall victim to impulsive purchases or carry credit card balances without much thought. However, educating oneself about the long-term implications of these choices can foster a new mindset—one rooted in intentionality rather than reaction.

Canadians can take a step back by incorporating simple reflective practices before making a purchase. Questions such as “Is this a need or a want?” or “How will this affect my overall financial plan?” can recalibrate an individual’s thinking and help them make informed choices that align with their financial goals. This thoughtful approach not only reduces stress and anxiety associated with financial decision-making but also promotes a sustainable lifestyle that thrives on discipline and control over one’s financial situation.

Increased financial literacy thus empowers individuals to embrace an-oriented viewpoint towards their finances, reducing the likelihood of future debt accrual. By understanding savings strategies, investing in educational resources, and making mindful financial choices, Canadians can create a robust foundation that fortifies against debt and propels them towards lasting financial security.

DISCOVER MORE: Click here to learn how to apply for the Amex Gold Rewards Card</

Conclusion

In today’s fast-paced, consumer-driven society, financial education emerges as a vital tool for preventing debt and securing a stable financial future. The lessons learned through mastering budgeting, savings, and investing can empower Canadians to navigate financial landscapes with confidence and foresight. By understanding the importance of creating an emergency fund, individuals are better prepared to handle unexpected challenges without falling into the trap of high-interest debt.

Moreover, the ongoing pursuit of financial literacy through community resources, workshops, and online platforms is essential. These resources provide insights into effective financial management, ensuring individuals are aware of opportunities and benefits that can contribute to their wealth-building endeavors. The understanding of various financial instruments, such as the RRSP and TFSA, further enhances one’s ability to make informed decisions that prioritize long-term gains over immediate gratification.

The cultivation of a mindful approach towards spending and decision-making is equally significant. By developing the habit of reflecting on purchases and setting clear financial goals, Canadians can shift their mindset from impulsivity to intentionality. This shift not only reduces the likelihood of debt but also fosters a more disciplined and secure financial environment.

Ultimately, financial education stands as a cornerstone in the quest for debt prevention. By embracing its principles and practices, Canadians can pave their way towards achieving not just financial stability but also a sense of empowerment and control over their economic futures. In this journey, knowledge truly becomes the first step towards financial freedom.

Linda Carter

Linda Carter is a writer and financial expert specializing in personal finance and financial planning. With extensive experience helping individuals achieve financial stability and make informed decisions, Linda shares her knowledge on the our platform. Her goal is to empower readers with practical advice and strategies for financial success.