The Impact of Credit Card Interest Rates on Consumers’ Financial Health

The Impact of Credit Card Interest Rates on Consumer Finances

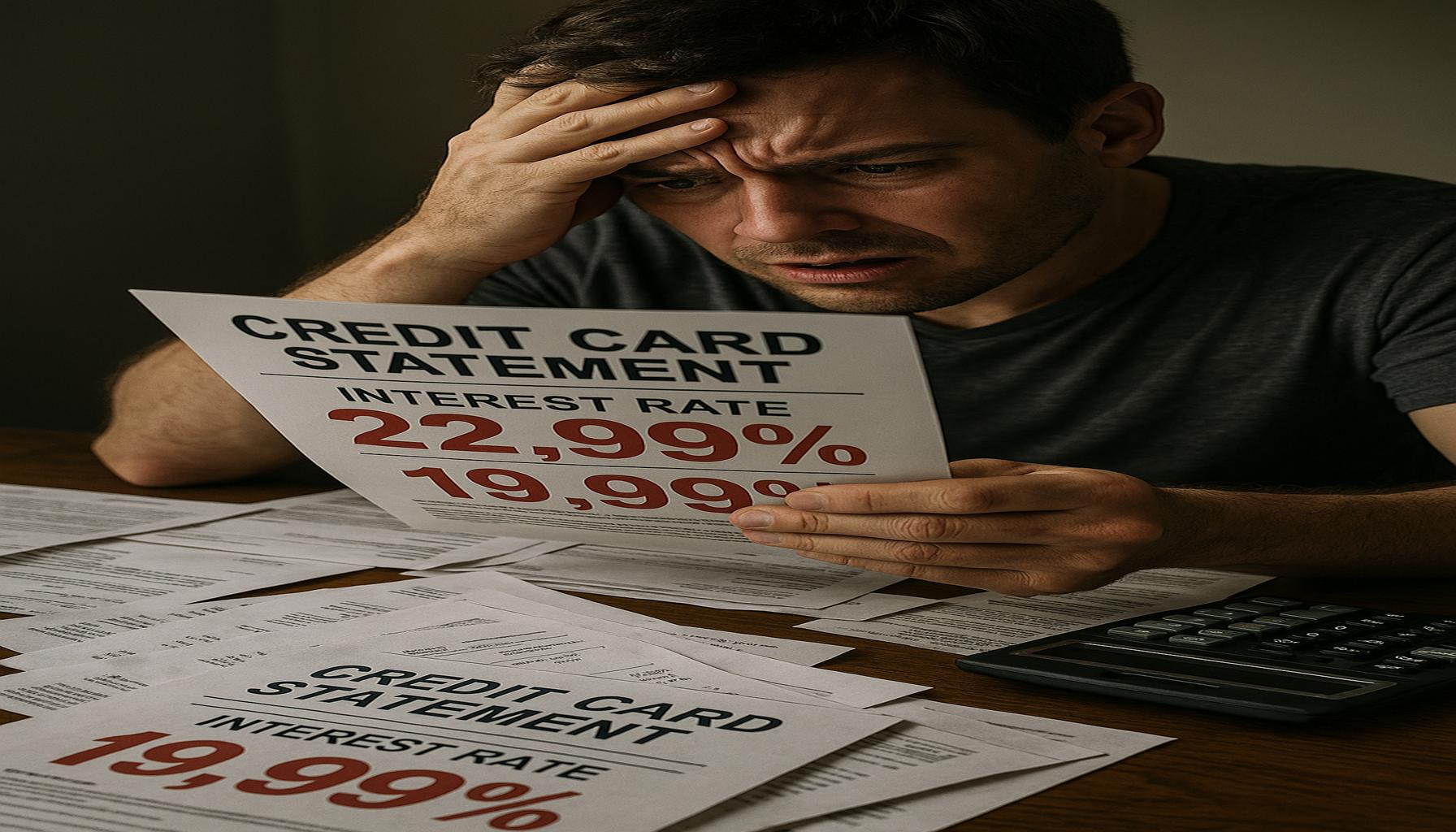

For many Canadians, credit cards are not just a means of payment; they are a critical part of their financial landscape. While these cards offer the convenience of immediate purchasing power, the interest rates attached to them can pose significant challenges, especially in a climate of rising living costs and shifting economic conditions. Understanding how these rates operate can help consumers mitigate their impact on financial health and overall quality of life.

The burden of credit card interest can be overwhelming. When balances remain unpaid, high interest costs accumulate rapidly. For example, if a Canadian borrows $5,000 on a credit card with a 20% annual interest rate and only pays off the minimum amount each month, they could potentially end up paying hundreds, if not thousands, more in interest over time. This scenario highlights how quickly debt can spiral out of control, making it increasingly difficult to reach financial stability.

Additionally, many consumers find themselves caught in a minimum payments trap. Making only the minimum payment can feel tempting, especially in challenging economic times. However, this strategy prolongs the repayment period significantly, leading to larger total debt figures due to ongoing interest accumulation. For instance, a person with a $2,000 balance at a 19% interest rate may take years to pay it off while ultimately paying nearly double the original amount in interest alone if only the minimum monthly payments are made. It’s essential for individuals to recognize this trap and take proactive steps to avoid it.

The implications of high credit card balances extend beyond immediate financial concerns; they can also harm one’s credit score. When consumers carry high balances relative to their overall credit limit, their credit utilization ratio increases. A high ratio can significantly reduce credit scores, impeding their ability to secure loans or mortgages in the future. For Canadians looking to purchase homes or finance education, maintaining a healthy credit score is crucial for accessing favorable interest rates and terms.

In a nation where personal debt levels continue to rise, understanding the consequences of credit card interest rates is more important than ever. Consumers should regularly assess their spending habits, consider lower interest options, and explore strategies for managing balances more effectively. This includes shopping around for credit cards with more favorable rates, utilizing balance transfer offers, and setting strict budgets to prevent overspending.

As we delve deeper into the topic, it becomes clear that the effects of credit card interest rates resonate beyond financial figures. They can influence stress levels, family dynamics, and overall life satisfaction. Staying informed and proactive enables consumers to make better financial choices that lead to lasting stability and improved quality of life. With the right approach, Canadians can navigate their financial journeys with confidence and success.

DISCOVER MORE: Click here to learn how to make the most of your credit cards

Understanding the Burden of Credit Card Debt

The psychological and financial ramifications of high credit card interest rates can take a significant toll on consumers in Canada. When faced with rising costs for everyday essentials, a growing number of Canadians resort to credit cards to bridge the gap. This reliance on credit can quickly lead to a situation where debt begins to feel insurmountable, particularly when paired with high interest rates that can exceed 20%. The reality is that while credit cards offer a convenient financial solution in the short term, their long-term impact can severely hinder financial health.

One core issue is the compounding effect of credit card interest. Each month, interest is calculated on the remaining balance, meaning that even small purchases can lead to considerable debt over time. For example, if a consumer purchases a few items totaling $500 and does not pay off the balance, the interest incurred on that amount can grow exponentially, leading to a much higher debt burden than initially anticipated. Understanding this feature is vital for consumers as they strategize their financial management.

Moreover, the psychological burden of carrying credit card debt often leads to increased stress and anxiety. Many consumers feel trapped as they navigate the dual pressures of daily expenses and outstanding credit card bills. This cycle can have detrimental effects not only on personal finances but also on mental and emotional well-being. As financial strain increases, relationships and personal life may suffer, leading to a downward spiral that can make finding a way out of debt even more challenging.

To combat the effects of high interest rates, consumers should consider several proactive strategies:

- Create and adhere to a strict budget to prevent overspending and prioritize debt repayment.

- Explore lower interest credit options or cards that offer promotional interest rates, making repayment more manageable.

- Pay more than the minimum monthly payment whenever possible to reduce both the remaining balance and interest accrued.

- Consider debt consolidation through personal loans or balance transfer offers that carry lower interest rates.

By recognizing the influence of credit card interest rates on overall financial well-being, consumers can exercise greater control over their financial futures. Awareness of these factors is the first step toward making informed decisions that safeguard their financial health.

As the conversation on consumer debt continues, it becomes increasingly clear that the overarching effect of credit card interest rates has implications that extend far beyond just monetary value. Understanding these dynamics can empower Canadians to navigate their financial challenges, ultimately leading to a balanced and healthier life.

DON’T MISS OUT: Click here to learn how to negotiate your bills

The Ripple Effects of Credit Card Interest Rates

The implications of high credit card interest rates extend far beyond mere financial strain; they permeate various aspects of consumers’ lives, creating a ripple effect that can impact long-term financial security. One of the most concerning effects is how it stifles the ability to save for the future. When a significant portion of disposable income is allocated to servicing credit card debt, opportunities for saving, investing, and preparing for emergencies diminish. In fact, according to a recent Canadian Financial Capability Survey, nearly 40% of Canadians reported they would struggle to cover unexpected expenses, largely because of overwhelming debt obligations. In such a climate, individuals may find themselves living paycheck to paycheck, unable to build a safety net that can absorb financial shocks.

Additionally, high credit card balances and their accompanying interest payments can hinder the ability to qualify for larger loans, such as mortgages or vehicle financing. Lenders scrutinize debt-to-income ratios, and an elevated credit card balance can signal financial instability. This reality poses a significant barrier for consumers looking to achieve milestones like homeownership or starting a business. A solid credit score, often tarnished by revolving credit balances, means fewer options for accessing capital when it’s needed most. Such struggles can create a vicious cycle where consumers are forced to rely on credit cards for necessities while being unable to improve their financial circumstances.

Moreover, the increasing reliance on credit can lead to a false sense of security. Consumers may feel they can navigate their financial situation by simply charging items to their credit cards, losing track of the reality created by interest accumulation. For example, making only the minimum payment on a credit card can lead to the total cost of a purchased item ballooning far beyond its original price. This false security often leads to increased spending on non-essential goods, contributing to a worsening debt cycle.

Long-term reliance on credit cards can also have social ramifications. It’s not uncommon for individuals burdened by credit card debt to prioritize repayment over social engagements, resulting in isolation. The anxiety and shame associated with financial struggles can breed reluctance to seek help or advice from friends and family, which could otherwise provide valuable emotional support or financial guidance. A sense of community and connection often plays a crucial role in overall well-being, and when debt drives a wedge between individuals and their support networks, the psychological toll intensifies.

To navigate these challenges effectively, consumers must embrace financial literacy as an essential skill. Understanding how interest rates work, recognizing the true cost of carrying credit card balances, and learning practical budgeting techniques can empower Canadians to reclaim control over their financial destinies. Access to reliable resources, such as financial counseling and educational programs aimed at improving financial literacy, can be a game-changer in the fight against the detrimental effects of high-interest credit cards.

Ultimately, being proactive in addressing personal debt and interest rates not only fosters individual resilience but also contributes to building a financially healthier society. As more Canadians become informed about the impact of interest rates, they can collectively work towards a culture that promotes sound financial practices and improves overall well-being.

DISCOVER MORE: Click here for complete application details

Conclusion

In summary, the impact of credit card interest rates on consumers’ financial health is profound and multifaceted. As explored throughout this article, high interest rates not only strain individual finances but also complicate the broader, societal landscape of economic stability. The essence of financial health is built upon the ability to save, invest, and manage debt effectively—all of which are jeopardized by the escalating costs of credit. When a substantial portion of income is funneled into servicing debts, the likelihood of achieving essential life goals, such as homeownership or preparing for unforeseen expenses, diminishes significantly.

Furthermore, the psychological burden of credit card debt can result in feelings of isolation and anxiety, which further exacerbates financial struggles. This highlights the urgent need for enhanced financial literacy among consumers. By equipping themselves with knowledge regarding interest rates, budgeting tactics, and effective debt management strategies, Canadians can shift the narrative surrounding credit card use and reclaim control over their financial futures.

Recognizing the far-reaching ramifications of credit card interest rates invites a broader cultural dialogue about responsible credit usage. As we strive to foster a society where sound financial practices are the norm rather than the exception, embracing education and open communication about financial health becomes imperative. Therefore, it is vital to create an environment where individuals feel empowered to step out of the cycle of debt, contributing not only to their own well-being but also to a financially resilient community as a whole.

Linda Carter

Linda Carter is a writer and financial expert specializing in personal finance and financial planning. With extensive experience helping individuals achieve financial stability and make informed decisions, Linda shares her knowledge on the our platform. Her goal is to empower readers with practical advice and strategies for financial success.