The Importance of Financial Education in Preventing Indebtedness

The Importance of Financial Education

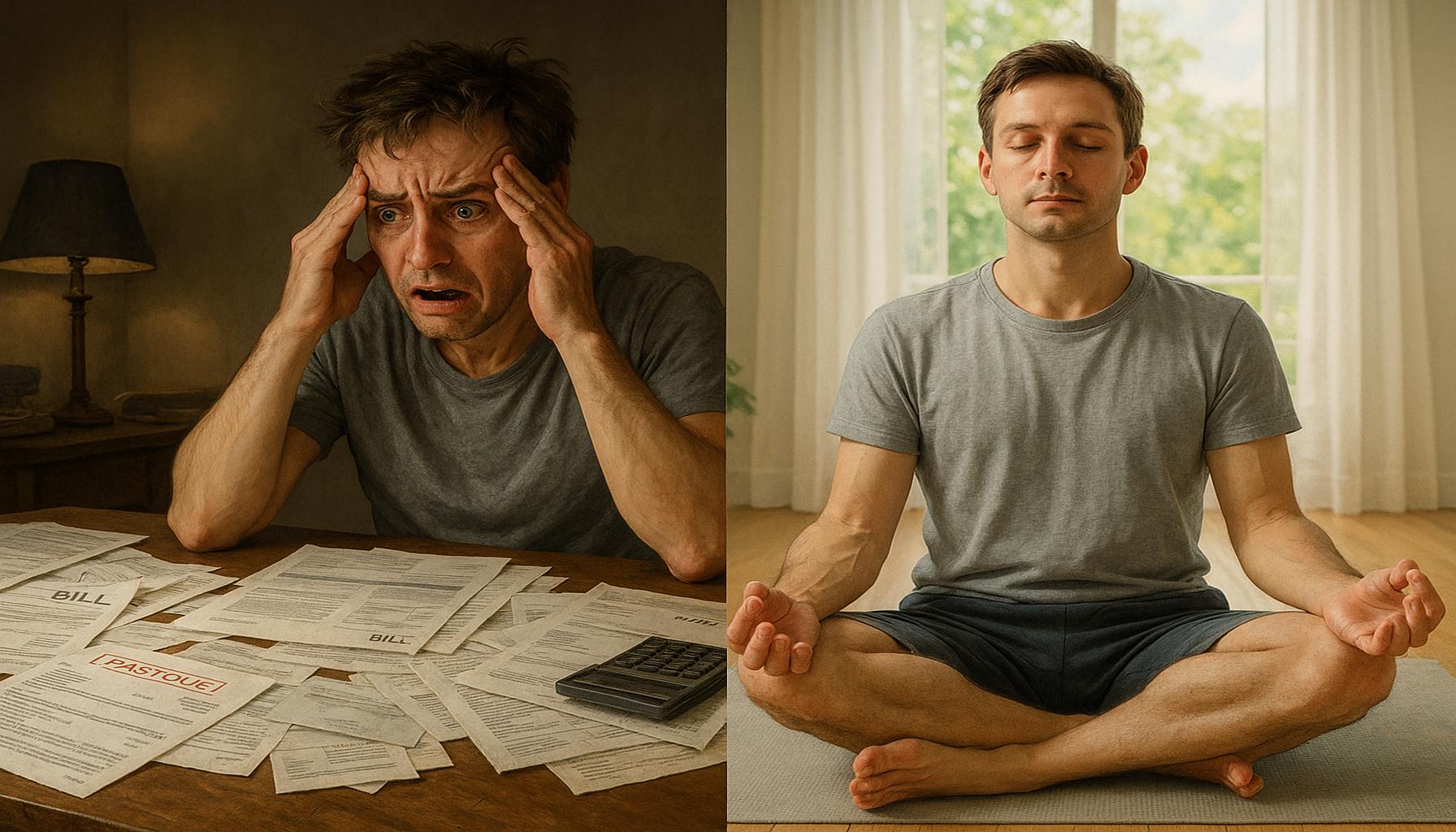

In an age characterized by rapid financial innovations and the increasing complexity of various financial products, having a solid foundation in financial education is pivotal. The prevalence of personal debt in the United States highlights the pressing need for individuals to understand their financial landscape; nearly 190 million Americans are grappling with some form of debt, which can include credit cards, student loans, mortgages, or medical bills. The emotional toll of financial insecurity is demonstrated by the fact that about 68% of American adults find themselves living paycheck to paycheck, amplifying the obligation to invest in financial literacy.

By empowering individuals through financial education, several critical outcomes can be achieved:

- Make informed financial decisions: A well-rounded understanding of essential financial concepts such as credit scores and interest rates enables individuals to make better decisions. For instance, someone who comprehends how their credit score affects loan approvals and rates may choose to improve it by paying down existing debt or making timely payments, thereby enhancing their financial opportunities.

- Avoid high-interest debt: Many consumers fall prey to predatory lending practices that can trap them in cycles of debt. For example, payday loans often have exorbitant interest rates exceeding 400%, which can create significant financial strain. Educated consumers are more likely to recognize red flags and opt for safer lending alternatives, such as credit unions or community banks that offer lower interest rates.

- Plan for the future: Financial literacy encourages individuals to save and invest, laying the groundwork for long-term financial security. A well-educated individual understands the importance of establishing an emergency fund, aiming for at least three to six months of living expenses, which acts as a monetary safety net and reduces stress during unforeseen situations.

Additionally, financial education extends far beyond mere understanding of basic concepts. It directly contributes to overall well-being in the following ways:

- Lower stress levels: Financial insecurity can lead to anxiety and stress. Those with a firm grasp of their financial situation often experience heightened peace of mind, knowing they are more prepared for any financial challenges that may arise.

- Improved credit scores: Individuals who educate themselves about their credit profiles are likely to practice behaviors that enhance their creditworthiness. Timely payments and responsible credit usage can result in favorable interests rates for loans and credit cards, allowing for significant savings in the long run.

- Better budgeting: Understanding the intricacies of budgeting can profoundly impact financial health. For example, individuals who learn to track their spending and differentiate between wants and needs are better equipped to allocate their resources efficiently. This practice not only helps facilitate necessary savings but also provides the ability to handle unexpected expenses without resorting to debt.

Investing time in financial education is essential for navigating the complexities of today’s financial world. By equipping individuals with the knowledge and skills to face fiscal challenges, we can cultivate a culture of financial responsibility. Such initiative fosters proactive engagement with personal financial management, enabling individuals to break free from detrimental cycles of debt and empowering them to thrive in their financial journeys.

DISCOVER MORE: Click here to learn how to declutter your life

Understanding Financial Products and Services

To enable individuals to make prudent financial decisions, it is crucial to delve into the myriad of financial products and services available in the market today. Many consumers may find themselves overwhelmed by options ranging from savings accounts to investment vehicles, loans, and insurance policies. Without the proper educational foundation, navigating this landscape can lead to unintended financial missteps that contribute to accumulating debt.

Understanding the terms and conditions associated with various financial instruments is of utmost importance. For instance, consider the difference between a secured loan and an unsecured loan. Secured loans, such as mortgages or auto loans, require collateral; if borrowers fail to repay these loans, lenders can claim the collateral. Conversely, unsecured loans do not involve collateral but often come with higher interest rates due to the increased risk for lenders. An informed individual who evaluates these distinctions can make choices aligned with their financial goals and risk tolerance.

- Interest rates: Grasping how interest rates function is vital. For instance, the average credit card interest rate in the U.S. hovers around 16%—a substantial cost for those who carry a balance. Understanding how these rates compound can motivate borrowers to pay down their balances swiftly, thereby avoiding excessive debt accumulation.

- Credit scores: A deep comprehension of credit scores and their implications is essential. Many individuals remain unaware that a score below 620 is typically classified as subprime, resulting in higher borrowing costs. Financial education empowers consumers to manage their credit behaviors effectively, promoting timely payments that enhance their scores.

- Fees and penalties: Various financial products come with fees and penalties that can significantly impact an individual’s budget. From overdraft fees on checking accounts to late payment charges on loans, understanding these costs can lead to better management practices that avert unnecessary debt.

Additionally, financial education informs consumers about predatory lending practices that can lead to crippling debt. Unlicensed lenders often target vulnerable populations, offering loans with exorbitantly high interest rates and hidden fees that entrap borrowers in a cycle of debt. Knowledge of these exploitative tactics equips individuals to recognize and evade these perilous financial traps, ultimately preserving their financial integrity.

Furthermore, exploring the importance of having a well-constructed budget can have profound implications for one’s financial health. A comprehensive budget enables individuals to track income and expenditures, ensuring that they live within their means. Educated individuals distinguish necessary expenses from discretionary spending, which facilitates the ability to allocate funds toward savings or investments rather than impulsive purchases that may lead to debt.

Building a budget necessitates not just an awareness of current expenses, but also an anticipation of future needs. Factors such as retirement savings, educational expenses, and emergency funds require careful planning. Establishing a proactive approach toward these financial elements reduces the likelihood of falling into debt when unexpected expenses arise or when planning for long-term goals.

In summary, financial education serves as the backbone of sound financial decision-making. By fostering a thorough understanding of financial products, interest rates, credit scores, and budgeting strategies, individuals are better equipped to navigate the financial landscape and avoid burdensome debt. It empowers them to make wise choices that promote financial security and well-being, effectively curbing the risk of indebtedness.

DISCOVER MORE: Click here to learn how minimalism can change your life

The Role of Financial Literacy in Debt Management

Beyond understanding financial products, the significance of financial education in debt management cannot be overstated. With the proliferation of consumer debt in the United States, which totals approximately $16 trillion according to the Federal Reserve, it is imperative that individuals acquire the skills necessary to navigate the complexities of personal finance to avoid falling into precarious financial situations. Financial literacy equips consumers to recognize their borrowing limits, manage existing debts, and develop strategies for successful debt repayment.

A key element in managing debt is knowing how to prioritize expenses effectively. Financial education guides individuals in understanding their debt obligations—such as credit card debts, student loans, and personal loans—and helps them implement a structured repayment plan. For example, the debt avalanche method focuses on paying off debts with the highest interest rates first, saving money over time on interest payments. Conversely, the debt snowball method, which emphasizes paying off the smallest debts first, may provide psychological benefits as individuals see quick wins, encouraging further responsible financial behavior. Both methods emphasize the importance of developing a repayment strategy tailored to individual circumstances, showcasing how education can foster effective debt management.

Moreover, understanding the concept of interest accumulation is vital for avoiding debt traps. For instance, many consumers remain unaware that carrying a balance on their credit cards can lead to costs ballooning due to high interest rates and fees. According to CreditCards.com, the average American household with credit card debt owes around $15,654. By grasping how interest accrues and influences total repayment amounts, individuals are more likely to pay off their balances promptly, thereby minimizing the total cost of borrowing.

- Emergency Preparedness: A comprehensive financial education also stresses the importance of establishing an emergency fund, which serves as a financial safety net. Having three to six months’ worth of living expenses saved can prevent the need to rely on credit during unforeseen circumstances, such as job loss or medical emergencies. This proactive measure helps individuals avoid the cycle of accruing debt during tough times.

- Investment in Knowledge: Continuous education and financial self-improvement can lead to better money management practices. Understanding the impact of overall consumer behavior, such as impulse buying and lifestyle inflation, can help individuals make more conscious spending decisions. Such behavioral insights can deter individuals from acquiring unnecessary debt.

Additionally, financial education encourages responsible use of credit. While credit can be a useful tool for building a favorable credit history and providing necessary funds for significant purchases like homes or vehicles, lack of awareness regarding its misuse can lead to profound consequences. According to Experian, approximately 30% of Americans have defaulted on a debt at some point, indicating a clear lack of wisdom in borrowing practices. Insights into responsible credit use—like maintaining a credit utilization ratio below 30%—can aid consumers in forging and sustaining strong credit profiles while avoiding default.

Furthermore, educational programs that focus on understanding financial aid options can play a pivotal role in preventing student loan debt. Many students remain unaware of scholarship opportunities, grants, or alternative financing options that could minimize their debt burden upon graduation. By fostering a mindset focused on informed choices, learners can pursue educational goals without accruing substantial loans, thus building a stable financial future.

In conclusion, financial education serves as an essential instrument in debt management by imparting knowledge about payment strategies, interest accumulation, budgeting, and responsible credit use. This understanding equips individuals to navigate financial landscapes prudently, cultivate positive financial habits, and ultimately steer clear of the pitfalls of excessive indebtedness.

LEARN MORE: Click here to discover the power of detachment

Conclusion

In summary, the critical importance of financial education in preventing indebtedness cannot be overstated. As the landscape of personal finance grows increasingly complex, individuals equipped with a robust understanding of financial principles are better positioned to make informed decisions that promote financial stability. Through comprehensive education, individuals learn to establish budgeting techniques, recognize the dangers of high-interest debt, and prioritize their financial obligations effectively. Such knowledge is pivotal in developing sound repayment strategies—be it through the debt avalanche or debt snowball methods—ensuring that they can approach their financial challenges with confidence.

Furthermore, by fostering an awareness of interest accumulation and the importance of maintaining a healthy credit profile, education acts as a shield against the pitfalls of consumer debt. Recognizing the potential perils associated with impulsive spending and ineffective debt management, financially literate individuals are more likely to cultivate practices that minimize the risk of falling into cycles of debt. This proactive approach extends to preparing for unexpected events through the establishment of emergency funds and engaging in continuous self-education to enhance financial practices.

Ultimately, empowering consumers with the tools and knowledge necessary to navigate their financial journeys is fundamental in combating the growing issue of indebtedness in the United States. By prioritizing financial literacy, individuals not only pave the way for their personal financial success but also contribute to a more financially savvy society, fostering resilience against economic uncertainties that can lead to debt accumulation.

Linda Carter

Linda Carter is a writer and financial expert specializing in personal finance and financial planning. With extensive experience helping individuals achieve financial stability and make informed decisions, Linda shares her knowledge on the our platform. Her goal is to empower readers with practical advice and strategies for financial success.