Credit Cards for Students: How to Build a Credit History Early

Understanding Credit Cards for Students

Getting your first credit card as a student is a pivotal step towards building a strong financial future. With responsible usage, a credit card can help you establish a solid credit history, which is crucial for future financial endeavors. As you embark on this new journey, it is essential to comprehend the significance of your credit history and how to manage your card wisely.

Why is credit history important? Consider the following points:

- Loan Approval: A good credit score increases your chances of being approved for loans. Whether you’re looking to buy a car or secure a mortgage, lenders will scrutinize your credit history. For instance, data compiled by Experian reveals that individuals with high credit scores (740 and above) often receive more favorable loan approvals compared to those with lower scores.

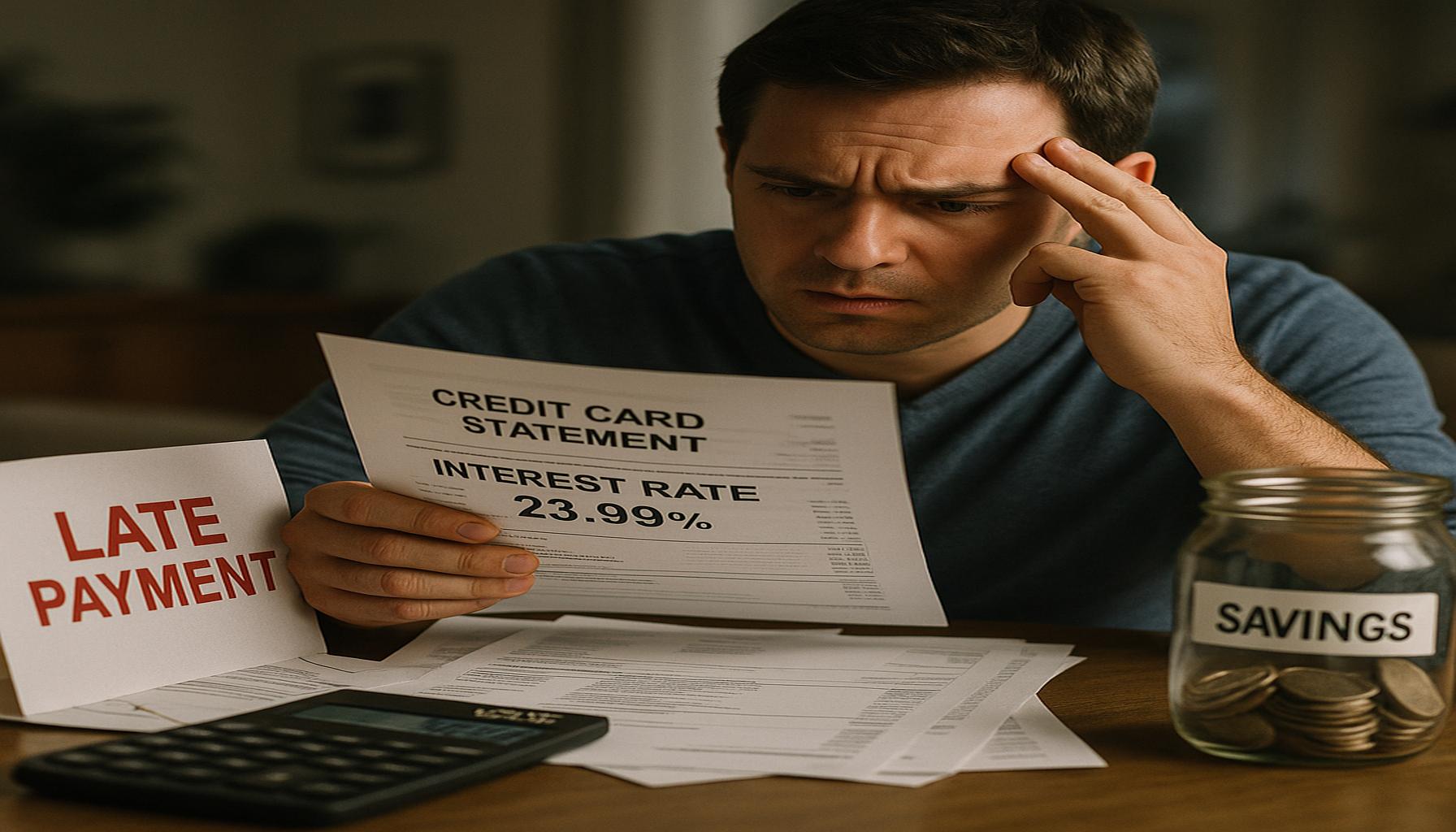

- Interest Rates: Positive credit history often leads to lower interest rates on loans and mortgages. According to the Consumer Financial Protection Bureau, a higher credit score can result in potential savings of thousands of dollars over the life of a loan due to lower interest rates. For students, a credit card can establish that positive history early on.

- Insurance Premiums: Many insurers utilize credit scores to determine premiums. It has been shown that individuals with better credit scores may pay significantly lower premiums, which can add up to substantial savings each year.

As a student, you may wonder which credit cards are suitable for your unique situation. Here are some features to consider:

- No Annual Fees: Opt for cards that don’t charge yearly fees. Many student credit cards are designed with this in mind, making them ideal for limited budgets. This allows students to build credit without incurring unnecessary costs.

- Reward Programs: Some cards offer rewards for purchases, such as cashback on groceries or dining. For example, the Discover it® Student Cash Back card provides 5% cashback in rotating categories, which can be particularly beneficial for students who spend money in those categories throughout the year.

- Student-Friendly Policies: Look for cards designed specifically for students, which often come with lower credit limits and lenient approval requirements. These considerations help you manage your spending effectively while still embarking on responsible credit usage.

Understanding how to leverage a credit card effectively will set you up for financial success. It’s vital to make informed decisions about payment methods and timely repayments to maintain your credit score. Regularly monitoring your credit report is equally important, as it helps catch errors that may affect your score. In conclusion, with careful management and the right choice, a student credit card can be a valuable tool in establishing a solid financial foundation for the future.

DISCOVER MORE: Click here for practical tips on minimal living

Choosing the Right Credit Card for Your Financial Journey

When it comes to selecting a credit card as a student, understanding the various options available is paramount. Not all credit cards are created equal; some are tailored specifically for students, which means they often come with specific features designed to help you manage your credit more effectively. In this section, we will delve into the desirable components of student credit cards and look at some key considerations to help you find the best fit for your financial goals.

Key Features of Student Credit Cards

There are several features students should prioritize when reviewing credit cards:

- Low or No Interest Rates: A competitive interest rate is essential, especially for those who may not be able to pay off their balance in full each month. Cards with significantly high interest rates can lead to substantial debt if you carry a balance, so seek out those with rates below the national average, which can often be found in student-friendly cards.

- Flexible Payment Plans: Some credit card issuers offer flexibility in payment plans, allowing students to pay off their balances in more manageable increments. This flexibility can alleviate financial stress and encourage responsible credit use, reinforcing good habits.

- No Annual Fees: Many student credit cards do not charge an annual fee, which is a budget-friendly option for students on tight budgets. Avoiding these fees ensures that you can focus on building credit without worrying about additional costs cutting into your finances.

- Rewards and Cashback: Credit cards offering rewards or cashback on various categories—such as dining, groceries, and fuel—can maximize the value you receive from your spending. For example, the Chase Freedom Student Credit Card offers 1% cashback on all purchases and additional rewards for specific categories. This can help you save money over time, especially if you utilize your card for routine expenses.

The Impact of Responsible Usage

Once you choose a suitable card, understanding how to use it responsibly is crucial to building a positive credit history. Here are some key practices to adopt:

- Pay Your Bills On Time: Consistently paying your credit card bill on or before the due date is one of the most vital factors contributing to your credit score. Late payments can incur fees and significantly lower your score, which may hinder your ability to secure loans in the future.

- Keep Your Credit Utilization Low: Aim to use no more than 30% of your available credit limit at any given time. For example, if your credit limit is $1,000, try to keep your balance below $300. Lower credit utilization ratios are viewed positively by lenders and can enhance your credit score.

- Monitor Your Credit Report: Regularly reviewing your credit report can help you understand how your credit behavior affects your score. In the United States, you are entitled to one free credit report each year from each of the three major credit bureaus—Equifax, Experian, and TransUnion.

In summary, selecting the right credit card embedded with favorable terms and utilizing it responsibly lays the groundwork for a solid credit history. Understanding these aspects paves the way for financial success, setting you up for a future filled with possibilities, such as favorable loan rates and improved financial security.

DISCOVER MORE: Click here to learn about the benefits of minimalism

Maximizing Benefits and Avoiding Pitfalls

While choosing the right credit card is a significant first step, understanding how to fully leverage its benefits and avoid common pitfalls ensures that students can effectively build and maintain their credit history. The following strategies and insights are critical in navigating the complexities of credit card usage while preventing detrimental financial missteps.

Understanding Interest Rates and Fees

Students must be acutely aware of the interest rates associated with their credit cards. According to a report by the Federal Reserve, the average interest rate on credit cards in the U.S. was around 16% as of 2023. For students who may retain a balance month-to-month, even a seemingly low interest rate can lead to significant costs over time. Therefore, prior to committing to a card, it is critical to compare different offers to find the best APR available and to understand the true cost of borrowing over an extended period.

In addition to interest rates, be vigilant about potential fees that could diminish your financial flexibility. Some cards charge foreign transaction fees, late payment penalties, or cash advance fees, which can all accumulate quickly. Utilize comparison websites like NerdWallet or Bankrate to identify credit cards that offer low fees or even waive them altogether for students. This approach not only saves money but also encourages smarter spending habits.

Building a Credit Mix

While having a credit card is essential, students can also benefit by diversifying their credit profile to include other types of credit, such as student loans or a secured loan. A credit mix (the variety of credit accounts) accounts for about 10% of your FICO credit score. Incorporating different types of credit can demonstrate to lenders your ability to manage various financial obligations responsibly. However, it’s crucial to not take on debt that is unnecessary or unmanageable just for the sake of improving your credit score.

Utilizing Automatic Payments and Alerts

To ensure timely payments, students can set up automatic payments for at least the minimum balance due. Many credit card issuers offer this option, which minimizes the risk of late payments and helps establish a habit of financial discipline. Additionally, subscribing to text or email alerts for payment due dates can provide a helpful reminder. With 60% of Americans reporting late payments as a primary source of debt-related stress, taking proactive measures against missed payments can mitigate this risk significantly.

Taking Advantage of Credit Education Resources

Many credit card issuers now offer valuable educational resources tailored specifically for students. For example, Capital One has developed the Smart Money Habits program, which offers tips and tools for managing credit. Engaging with these resources not only enhances understanding but reinforces the importance of responsible credit use. Furthermore, numerous non-profit organizations also provide workshops on personal finance management and credit education, which can be vital in preparing students for their financial future.

Debt Management Strategies

Lastly, students should develop strategies for debt management early. This might include creating a detailed budget that allocates funds for monthly expenses, debt repayment, and emergency savings. Studies show that individuals who maintain a budget are 80% more likely to be financially stable. By tracking spending habits and making adjustments as necessary, students can ensure that they remain within their means while still building their credit history.

Overall, students have the opportunity to not only establish their credit early on but to do so wisely, paving the way for a financially secure future. By maximizing the benefits of their credit cards, understanding the nuances of credit management, and avoiding common pitfalls, they can cultivate a credit profile that benefits them in the years to come.

DISCOVER MORE: Click here for tips on creating a capsule wardrobe

Conclusion

In conclusion, the journey of building a credit history as a student is a significant financial milestone that can set the foundation for future financial independence and success. By choosing the right credit card, students can take the first crucial step towards establishing their credit profile. However, it is equally important to remain vigilant about interest rates, fees, and the overall management of credit to avoid pitfalls that may hinder their financial progress.

Moreover, understanding the importance of a diverse credit mix, timely payments, and effective budget management can greatly enhance a student’s ability to build a robust credit history. Engaging with educational resources from credit card issuers and financial institutions helps reinforce knowledge and encourages informed decision-making. By adopting proactive debt management strategies, students can navigate the often complex world of credit with greater confidence.

Ultimately, establishing a healthy credit history doesn’t just benefit students in the short term; it opens doors to better financial opportunities in the future, including favorable loan terms, lower insurance premiums, and increased chances of credit approval. As students embark on this journey, it is crucial to remember that responsible credit usage is not just about borrowing; it is about laying the groundwork for a stable financial future. With diligence and informed choices, students can effectively build their credit history early, ensuring long-term financial well-being.

Linda Carter

Linda Carter is a writer and financial expert specializing in personal finance and financial planning. With extensive experience helping individuals achieve financial stability and make informed decisions, Linda shares her knowledge on the our platform. Her goal is to empower readers with practical advice and strategies for financial success.